What Happens When You Consolidate Your Debt?

Understanding Debt Consolidation

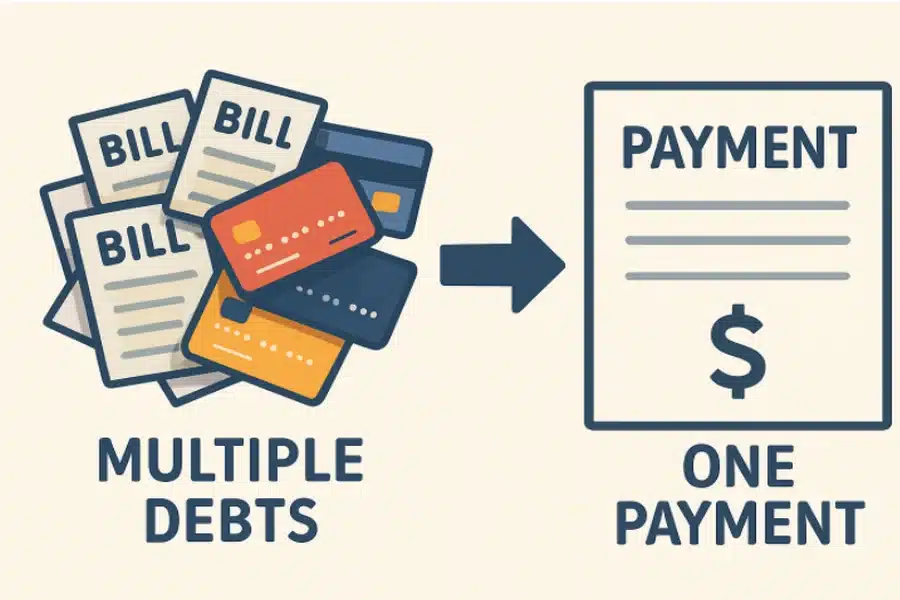

Debt consolidation brings multiple debts—such as credit cards, medical bills, and personal loans—into a single, streamlined payment. This strategy aims to simplify your financial life, potentially lower your interest rates, and help you stay on track with repayment. By consolidating, you’re not just reducing the stress of juggling several due dates but also opening up the chance to save money in the long run. For many individuals, seeking advice or assistance from industry professionals, such as Symple Lending, can be a smart first step in exploring debt solutions tailored to their specific needs.

The main approaches to debt consolidation vary depending on your financial profile and existing debts. Whether you use a personal loan, transfer your credit card balances, or tap into home equity, consolidation is all about putting your money to work more efficiently. Understanding how each method functions is critical, so you can make choices that align with your long-term financial health and avoid future pitfalls.

Definition and Purpose

Debt consolidation merges multiple debts into a single loan or payment plan. The primary goals are to simplify repayment and secure a more favorable interest rate. With a consolidated loan, you’ll face just one monthly obligation, making your budgeting process less complicated and reducing the risk of missed payments.

Common Methods

- Debt Consolidation Loans: Obtain a single, often unsecured, personal loan to pay off other outstanding debts.

- Balance Transfer Credit Cards: Transfer existing credit card balances to a new card with a promotional low or 0% interest rate for an introductory period.

- Home Equity Loans: Borrow against the equity in your home to pay off high-interest debts, typically resulting in lower interest rates.

As you consider these methods, it’s worth exploring information on companies that specialize in these solutions. Researching companies like Symple Lending provides valuable insight into your available consolidation paths and service options. Taking time to compare multiple providers can help you identify the most transparent and cost-effective option. Reading customer reviews and evaluating a company’s track record also ensures you make an informed choice.

Immediate Effects of Debt Consolidation

Simplified Payments

One of the noticeable effects of debt consolidation is the relief of managing just a single payment each month. This change streamlines your financial commitments, reducing administrative headaches and leading to better organization and timely payments.

Potential Interest Rate Reduction

Many debt consolidation products offer a lower interest rate than your previous debts, especially if your credit score has improved since you first obtained your loans. Lower rates mean a greater share of your payment goes toward principal, which can expedite your debt-free journey. Resources like U.S. News provide helpful insights on how to approach debt consolidation effectively and compare available options.

Impact on Credit Score

- Short-Term: Applying for a new loan or line of credit can cause a temporary dip in your score due to a hard inquiry.

- Long-Term: Regular, on-time payments to your consolidated debt may strengthen your credit score over time, reflecting positively on your credit history.

Long-Term Financial Implications

Total Interest Paid

Although your monthly payments may be lower with consolidation, extending the repayment period could increase your total interest cost. Carefully review your terms and compare the total repayment amount before you commit. Resources like CBS News highlight some surprising credit card debt consolidation benefits that can help borrowers better evaluate the trade-offs.

Credit Utilization Ratio

If you close old accounts after consolidation, your total available credit decreases, which may increase your credit utilization ratio and temporarily lower your credit score. Keeping old accounts open, even with zero balances, can help maintain a healthier score.

Behavioral Considerations

Without addressing underlying spending habits, there’s a risk you may accumulate additional debt. Effective debt consolidation requires a change in financial behavior to ensure long-term success.

Benefits of Debt Consolidation

Streamlined Finances

Having one consolidated payment per month helps make budgeting and money management more straightforward and less stressful.

Potential Cost Savings

By locking in a lower interest rate, you have a real chance of saving money over the life of your loan, reducing your total repayment burden.

Improved Credit Health

Consistent, timely payments on your new loan build positive credit history, which contributes to better credit health over time.

Risks and Considerations

Fees and Costs

Be aware of origination fees on loans or balance transfer fees with credit cards. These can add to your debt burden if not factored into your plan.

Secured vs. Unsecured Loans

Secured loans, such as home equity loans, use your property as collateral, which means failure to repay could result in foreclosure or asset loss.

Underlying Financial Habits

Lasting debt relief relies on disciplined money management. Without a budget and clear limits, you may fall back into unmanageable debt levels.

Steps to Effective Debt Consolidation

- Assess Financial Situation: Determine your total outstanding debts, current interest rates, and your ability to repay.

- Research Options: Compare rates, loan features, and any associated fees from various lending sources.

- Create a Repayment Plan: Build a realistic budget and commit to making timely payments each month.

- Monitor Credit Reports: Check your credit report regularly to track progress and ensure accuracy.

Alternative Strategies

Debt Management Plans

Partnering with a credit counseling agency can help you negotiate lower payments or interest rates, often without taking on new debt.

Debt Settlement

Debt settlement involves negotiating with creditors to pay a lump sum that is less than your total owed balance. Be aware, however, that this can impact your credit score and may have tax implications.

Bankruptcy

As a last resort, bankruptcy can discharge many debts, but it causes severe and long-lasting harm to your creditworthiness and should only be considered after other options have been exhausted.

Conclusion

Debt consolidation offers consumers a practical path to manage overwhelming debt through streamlined payments, lower interest rates, and potential credit health improvements. Yet, the effectiveness of consolidation relies on a clear understanding of its benefits and risks—and a real commitment to lasting financial habits. By choosing the right solution and maintaining discipline, you can regain control of your finances and move toward a debt-free future.