The Evolution of Hedge Fund Strategies in a Data-Driven Financial World

Hedge funds hold a specific place in modern institutional portfolios: they are expected to deliver differentiated returns when traditional models break down.

A broader industry discussion appears on bignewsnetwork.com, offering useful context for allocators evaluating today’s environment.

Understanding how hedge fund strategies generate alpha and why technology reshaped the industry has become essential for B2B investors working with hedge fund investing, hedge fund losses, and hedge fund average returns.

Why Hedge Funds Look Different Today

A defining shift of the last decade is the explosion of usable data. Funds equipped to process it gain advantages that intuition-led management cannot match. Systematic tools now sit at the center of decision-making, including real-time signal detection, automated execution, and layered risk controls.

In practical terms, this means lower behavioral bias and faster reaction speed. A macro fund that monitors thousands of indicators every day can adjust exposure within minutes during a volatility spike. Traditional methods rarely move that quickly.

Key point: alpha is increasingly engineered rather than improvised.

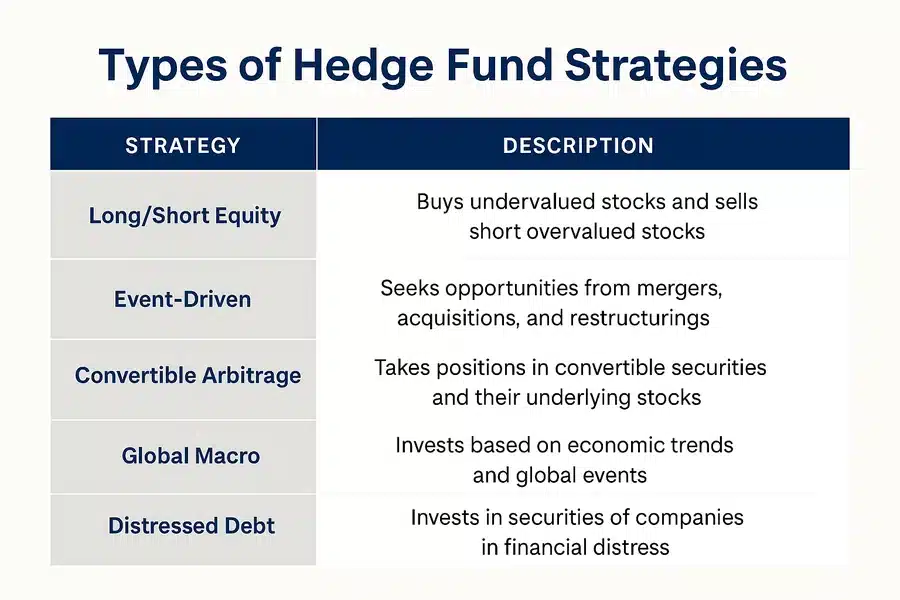

What Drives Alpha Across the Major Strategies

Long/short equity

Managers exploit valuation gaps by pairing long and short positions. A typical example is going long a discounted industrial supplier and short a more richly valued competitor. Because the return comes from relative pricing, the structure helps cushion drawdowns and supports institutions that want to limit hedge fund losses.

Event-driven

Corporate catalysts such as mergers or spin-offs create predictable spreads. A merger arbitrage discount of one or two percent seems small, but when repeated across dozens of positions, it becomes a steady income stream that is not closely tied to market mood.

Convertible arbitrage

By purchasing a convertible bond and shorting the corresponding equity, funds monetize volatility differences. The pricing gaps are subtle, yet properly hedged carry from small inefficiencies compounds significantly when a fund runs hundreds of positions.

Global macro

Macro managers express economic views across currencies, rates, equities, and commodities. When equity and bond correlations move in the same direction, macro exposure often becomes the only functional diversifier that still stabilizes a portfolio.

Distressed debt

Distressed specialists buy debt at deep discounts and rely on legal and restructuring expertise to capture recovery value. Historically, the approach has delivered strong risk-adjusted results in recessionary cycles.

Takeaway: each strategy exploits a different type of inefficiency, and combining them produces return patterns that traditional portfolios cannot replicate.

The Overlooked Risk: Operations

A surprising share of hedge fund failures originates in operations rather than investment decisions. Weak liquidity controls, inaccurate valuation procedures, or slow risk reporting can destroy capital more quickly than a mistimed trade. For that reason, sophisticated allocators examine areas such as redemption mechanics, counterparty concentration, and the speed of risk-system updates.

These factors determine whether hedge fund average returns will translate into real outcomes during a crisis.

Remember: strategy quality is meaningless without operational resilience.

When Hedge Funds Improve Portfolio Quality

For B2B investors such as insurers, pensions, and corporate treasuries, hedge funds matter most when they contribute something that core assets cannot. The value lies in uncorrelated returns, downside mitigation, flexible cross-asset positioning, and diversification that survives a stressed market.

When a classic 60/40 model fails because equities and bonds move together, long/short and macro strategies often provide the missing buffer.

How to Evaluate Allocations More Effectively

Institutions that consistently benefit from hedge fund investing tend to follow several discipline points. They perform deep operational due diligence. They select strategies that match portfolio objectives instead of chasing recent winners. They map liquidity carefully, including gates, lockups, and settlement cycles. They evaluate fees relative to long-cycle alpha, not short bursts of success.

Well-chosen hedge fund strategies do not replace core assets. They strengthen them.

Conclusion

Modern hedge funds reflect a shift toward systematic research, data-intensive processes, and institutional-scale risk frameworks. When chosen with clear strategic intent, they provide something that traditional portfolios increasingly lack. They offer resilient, uncorrelated performance during uncertainty. For organizations that manage complex liabilities or multi-asset mandates, hedge fund strategies represent not excitement, but stability, which is often the rarest asset when markets become unpredictable.